In early February 2008, I wrote this article giving my thoughts on 11 solar stocks. As you will recall, the stock market was hurting in January, and so were the solar stocks. In that article, I opined that the high-PE stocks in the group - First Solar (FSLR), SunPower (SPWR), and Suntech (STP) - were overpriced, while two were underpriced and screaming “BUY ME.” I further opined that if the market is truly rational, the investment returns on the low-priced stocks would exceed the returns from the high-PE stocks.

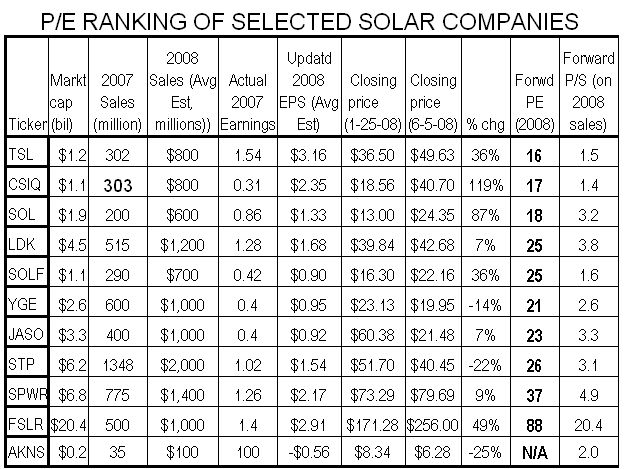

In that first article, I submitted a table I had put together, which calculated forward PE’s for 10 stocks in this space. The table is set out again below, with updated data as of yesterday’s close. As you can see, the market has been largely—but not completely—rational.

Canadian Solar (CSIQ), my favorite stock in January, is up a whopping 119% in a little over 4 months, its PE having increased from a ridiculously-low 11 in January to a more reasonable-but-still-attractive PE of 16 now. My second favorite stock in January—Trina Solar (TSL)—has turned in a respectable performance—up 36% as of yesterday, although it is down today. TSL released “interesting” earnings today and will be discussed in greater detail below.

ReneSola (SOL) actually IPO’ed (at $13.00) after I wrote my article and has also done very well—up 87% since January.

On the other hand, if you average the return on the three high-PE stocks I panned in January, you get an average return of 12%, with one of the three (STP) actually having dropped further since the pretty bad baseline in January.

FSLR did go up pretty substantially (49%), but far, far less than my favorite, CSIQ. Indeed, I believe FSLR is living on its previous laurels and momentum generated by all of its boosters in the investment community. I expect these high-PE stocks to continue to underperform their low-PE brethren going forward.

What has happened is precisely as it should be, in my opinion. FSLR is predicted to double its earnings between 2007 and 2008, and STP and SPWR aren’t even expected to do that, yet they trade at forward PE’s of 26 to 88. On the other hand, CSIQ and TSL are expected to more-than-double THEIR earnings in 2008, and yet their forward PE’s are 16-17. Of course, after today’s earnings report from TSL, I think the consensus for TSL earnings in 2008 will go up at least 10-15% from $3.16 to, putting TSL’s PE at about 12-13.

Solarfun (SOLF), Yingli (YGE) and JA Solar (JASO) trade at PE’s of 20-25, and I do not believe they offer more compelling values compared to TSL and CSIQ that would justify those higher PE’s. If a reader knows of a significant advantage one of these three has over TSL or CSIQ, please comment about it.

In my view, although SPWR is clearly the technology leader in the group today (they are cranking out 22% efficiencies in the lab, and are selling 19.3% efficient panels commercially), its growth rate has definitely decelerated. Indeed, on the conference call some weeks ago, SPWR indicated that revenues in Q2 of this year will be flat with Q1 (whereas TSL, for example, is guiding to about a 40% sequential increase in revenues). In my view, even given its technological prowess, and although it deserves some premium, SPWR is overpriced at a forward PE of 37. This is especially true given the fact that SPWR won’t even double earnings this year, while both TSL and CSIQ are expected to more than double their earnings. In addition, I believe other companies will substantially narrow the efficiency gap in the next year or two, decreasing SPWR’s relative advantage.

Suntech Power (STP) is also slowing in growth, with earnings only expected to go up 50% this year. I panned STP in January because I thought it was overpriced at its PE of 31, and I still think it is overpriced at a PE of 26, compared to CSIQ and TSL at about 14.

As to FSLR, I didn’t like its prospects in January, and I don’t like them any more now. For any company to justify a forward PE of 88, it has to be able to more than double its earnings on an annual basis for several years into the future, usually because it has a proprietary product or service for which there is no meaningful competition (think Microsoft OS’s in the distant past, although even in those days, I don’t think MSFT garnered forward PE’s of almost 100).

Although FSLR will probably double earnings this year, I doubt it will do so next year and the year after that. The expectations are so high that one tiny stumble and all of a sudden, FSLR no longer merits a forward PE of 88, and contraction of the multiple will hurt the stock price, or, at the very least, prevent any increase in stock price. One need not look far to find examples of this—look at STP and SPWR, both of which are trading at about half of their 52-week highs (AAPL and GOOG are two more examples of fabulous companies who got knocked down because they failed to meet continuing outrageous expectations—and they “only” trade at forward PE’s of 30 or so).

Frankly, I would not even pay a forward PE of 40 for FSLR, and here’s the reason why not:

The KEY reason FSLR is worth more than the other solars TODAY is because it is the price leader in terms of cost per watt. But there is only one reason for that price leadership—which is that polysilicon is priced in the hundreds of dollars per kilo, whereas within 2 to 3 years, it will be priced in the dozens of dollars (and not that many dozens at that). Since poly is the #1 manufacturing cost for FSLR’s competitors, an 80% decrease in the cost of poly (from, say, $250 to $50)—as is likely to occur over the next several years—will go very far towards eliminating FSLR’s cost advantage. Keep in mind also that FSLR also has one cost DISADVANTAGE that its poly brethren do NOT have—FSLR has to build TWO panels in order to generate the same amount of electricity that a SINGLE poly-based panel will make. That will double FSLR’s cost for aluminum, glass, manufacturing and other costs to build that extra panel.

When you take this into account, I would not be surprised if in three years, a single poly-based 300-watt panel costs no more to make than (2) 150-watt FSLR thin-film panels. And all things (including price) being equal, who wouldn’t prefer ONE 300-watt panel versus TWO FSLR 150’s? In other words, FSLR’s panels will actually have to be at least 15-20% cheaper just to induce purchasers to buy them because the amount of room they require and the extra installation costs will have to be compensated for.

Finally, how much upside is there for a company—any company—with a market cap of $20 billion? I simply don’t see 2-bagger potential for FSLR in the next year, whereas CSIQ and TSL with market caps of around a billion could double or triple in a year or two and still have a market cap FAR less than HALF that of FSLR TODAY. Another way to see this is to look at the price targets for FSLR, which range up to maybe $350 (I don’t follow this closely, so maybe I am wrong here). That gives FSLR an upside of maybe 40%. In contrast, if later in 2008, it looks like TSL will make $5.00/sh in 2009 (consensus before earnings release today was $4.19—see further discussion below), and by the end of 2008, TSL’s PE expands modestly to 18 against 2009 earnings, the resulting price of $90 represents a 2-bagger from the current trading price around $46.

In conclusion, I believe that the solar space will grow vigorously over the next decade, and I believe that at the present time, TSL and CSIQ continue to offer the best risk-reward ratio in this space. I do believe it’s difficult to look very far out (ie, beyond 2009) because I think by 2010, disruptive solar technologies (CIGS or other thin-film PV, concentrating photovoltaic, etc) will be sufficiently commercialized that they may present very serious competition to the polysilicon-based panel producers, but at this point in 2008, TSL, CSIQ and SOL offer the best prospects.

Finally, I want to discuss TSL’s earnings announcement this morning. The earnings headline number was $12.9 million, or 51 cents per share, slightly exceeding consensus of 48 cents, and substantially less than last quarter’s 62 cents. Not surprisingly, investors who did not look under the hood sold TSL today, causing it to drop to about $46 as I write this.

If one looked under the hood, however, one would discover a charge of $4 million against earnings due to “remeasurement of the non-US dollar denominated obligations in the US dollar functional currency”—whatever this means. In the absence of this weird charge that is apparently related to an accounting change that occurred for the first time this quarter, earnings would have been 67 cents. To put it a different way, if this accounting change had occurred next quarter, TSL would have announced earnings of 67 cents and the stock would be at $55 now rather than $46. Amazing how such an unanticipated and seemingly trivial decision can have such major impact.

Also, TSL paid over a million dollars in income taxes this quarter versus a tax benefit of half a million last quarter. Making a further adjustment for this would yield “operational” earnings (ie, earnings based on the sales and profit margins rather than currency exchange and income taxes) of about 75 cents this quarter.

More importantly, guidance for this year was increased—with operating margins of 15-17% expected on revenues of $770 to $808 million. Taking the midpoint on sales and margins ($789 million times 16%) yields operating income for this year of $126 million. Utilizing the same interest cost and exchange losses as just reported but annualizing them equals a cost of about $24 million and taxes at 4.92% (announced on the call) adds up to $6 million, yielding earnings in 2008 of $96 million, or $3.79/sh, yielding a PE of about 12 against the current trading price of about $46.

I believe that the analysts will go through the same math I have just done and that earnings estimates for both 2008 and 2009 will be increased by at least 10-15% in the next few days. Therefore, to me, TSL where it is trading now ($46) is a buy, not a sell.

To those not familiar with the solar space, I must close with a few cautions. First, solar stocks are EXTREMELY volatile, with 20% daily moves NOT unusual. So if you do not have the stomach for seeing your position lose 20% of its value in one day, solar may not be the place for you. Second, the solars have gone up a lot in the past few weeks, and there is a good argument to be made that they need to slide back before they go back up as we anticipate the next earnings season beginning next month. Third, there is reputed to be a psychological connection between oil prices and the solar stocks. To me, this was more of a factor in the past than it is now, but it remains a factor. Thus, if oil slides back from the $120’s, it may take the solars with it. Fifth, some people believe that the stock market in general may be heading back to 12,000 or even below to retest the Jan and March lows, and obviously, such a move may well impact the solars (although the solar often don’t follow the broader market on a day-to-day basis).

On the positive side, I think that there is a fair possibility that in the next few months, Congress may pass an energy bill that will extend the old incentives and create some new ones. Although some of that is already baked in, I believe the passage of this bill may move the solars up another 5-10%. Finally, especially if oil and gas hold up or even go higher, I believe that over the next few months we’ll hear more about factors that will be pro-solar—such as carbon-capture, increased state incentives spurred on by increases in the cost of electricity (due to higher costs of coal and natural gas) and due to environmental concerns, etc.

Whether the “bullish” forces I have discussed above beat the “bearish” ones, I cannot say. But if you are comfortable with the volatility and other risks discussed above, I think that TSL is a buy at $46 or $47 and CSIQ is a decent buy under $40.

No comments:

Post a Comment